Packaging manufacturer Ball (NYSE:BLL) reported Q2 CY2025 results exceeding the market’s revenue expectations, with sales up 12.8% year on year to $3.34 billion. Its non-GAAP profit of $0.90 per share was 3.8% above analysts’ consensus estimates.

Is now the time to buy Ball? Find out by accessing our full research report, it’s free.

Ball (BALL) Q2 CY2025 Highlights:

- Revenue: $3.34 billion vs analyst estimates of $3.12 billion (12.8% year-on-year growth, 7% beat)

- Adjusted EPS: $0.90 vs analyst estimates of $0.87 (3.8% beat)

- Adjusted EBITDA: $666 million vs analyst estimates of $501.7 million (20% margin, 32.8% beat)

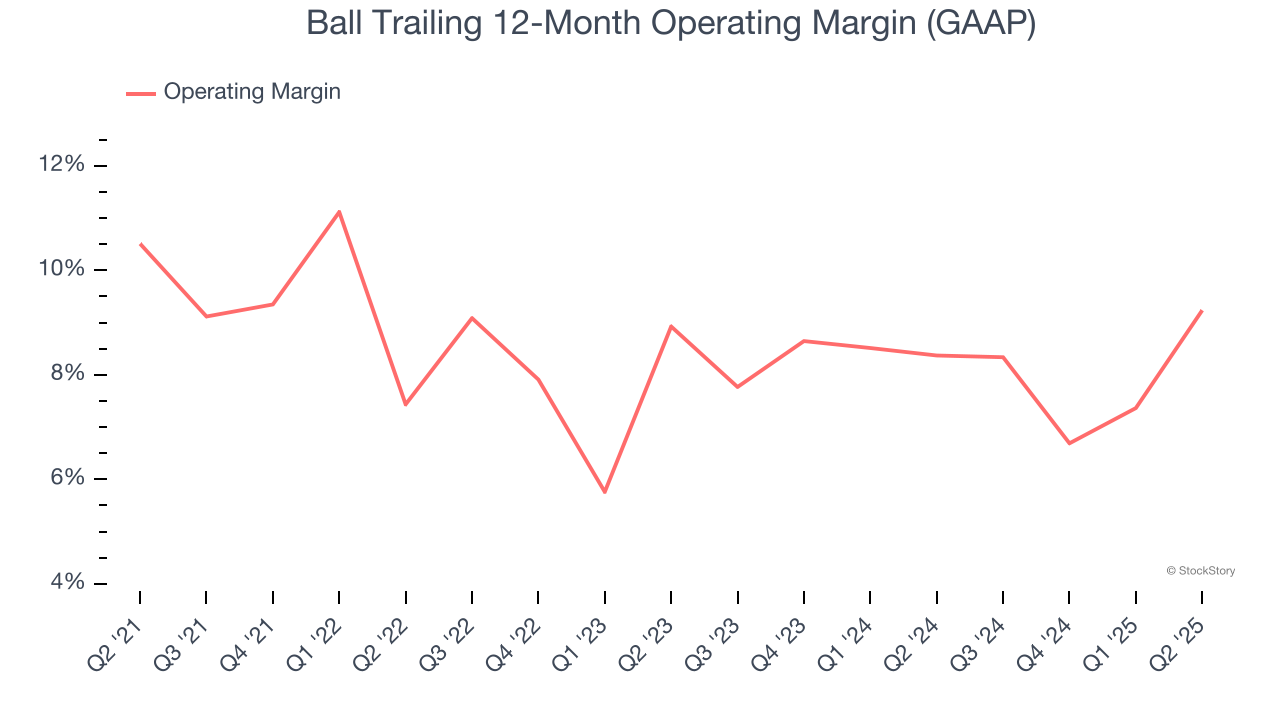

- Operating Margin: 15.3%, up from 8.5% in the same quarter last year

- Free Cash Flow Margin: 7.1%, up from 4.9% in the same quarter last year

- Market Capitalization: $15.98 billion

"We delivered strong second quarter results, returning $1.13 billion to shareholders in the first six months of 2025. Our robust financial position, leaner operating model, and focused growth strategy enabled us to achieve higher volume and increase our full-year guidance for comparable diluted earnings per share growth to 12-15%. While we remain mindful of potential geopolitical uncertainties and market volatility in the second half of the year, we are confident in our ability to achieve our 2025 objectives. Our ongoing commitment to operational excellence continues to drive manufacturing efficiencies, and our investments in innovation and sustainability are helping our customers better meet end-consumer needs, all while we tightly manage our cost structure. These actions position us well to navigate the near-term and consistently deliver long-term value to our shareholders," said Daniel W. Fisher, chairman and chief executive officer.

Company Overview

Started with a $200 loan in 1880, Ball (NYSE:BLL) manufactures aluminum packaging for beverages, personal care, and household products as well as aerospace systems and other technologies.

Revenue Growth

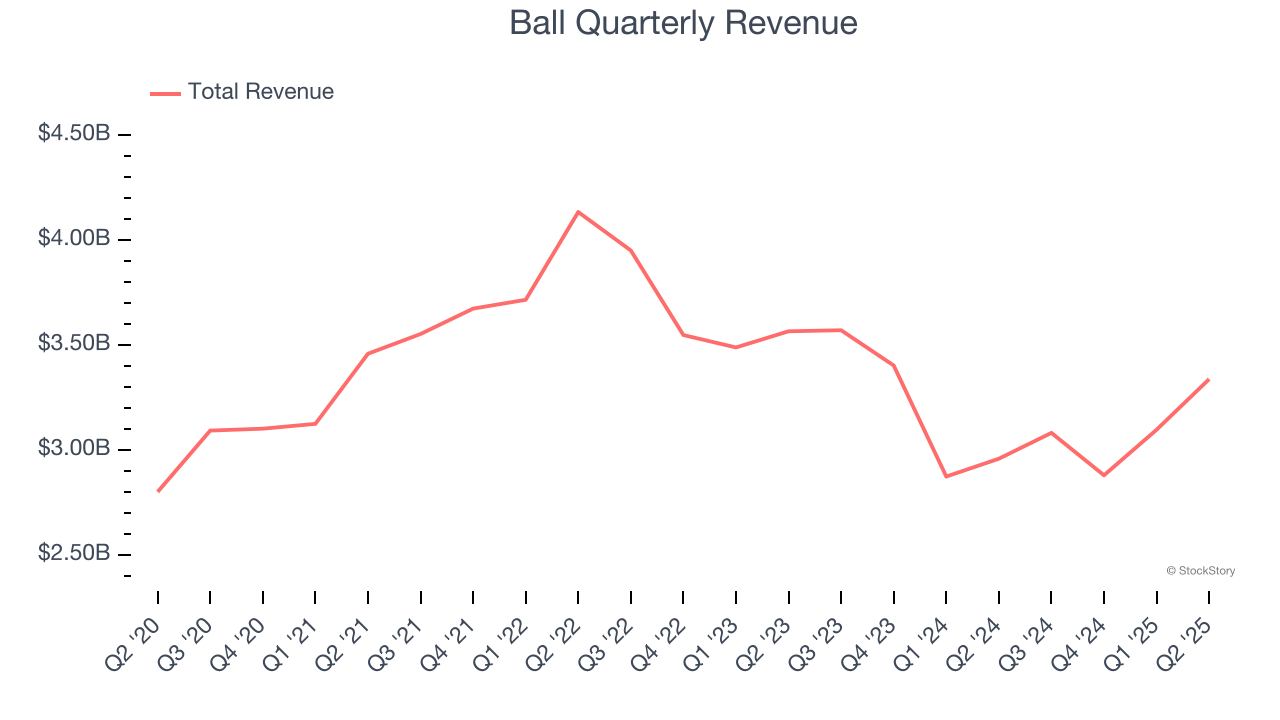

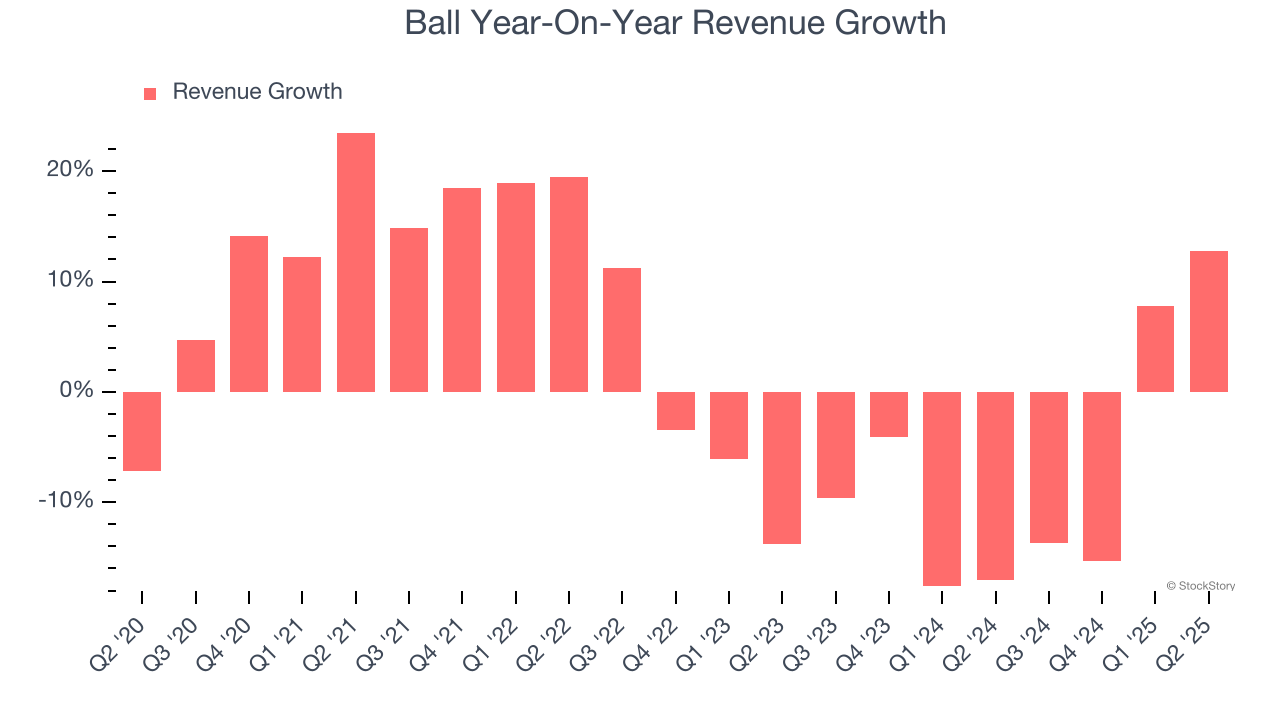

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Ball’s 1.9% annualized revenue growth over the last five years was sluggish. This was below our standards and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Ball’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 7.7% annually. Ball isn’t alone in its struggles as the Industrial Packaging industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

This quarter, Ball reported year-on-year revenue growth of 12.8%, and its $3.34 billion of revenue exceeded Wall Street’s estimates by 7%.

Looking ahead, sell-side analysts expect revenue to grow 2.4% over the next 12 months. While this projection implies its newer products and services will spur better top-line performance, it is still below the sector average.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Ball has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 8.8%, higher than the broader industrials sector.

Analyzing the trend in its profitability, Ball’s operating margin decreased by 1.3 percentage points over the last five years. Many Industrial Packaging companies also saw their margins fall (along with revenue, as mentioned above) because the cycle turned in the wrong direction. We hope Ball can emerge from this a stronger company, as the silver lining of a downturn is that market share can be won and efficiencies found.

This quarter, Ball generated an operating margin profit margin of 15.3%, up 6.8 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

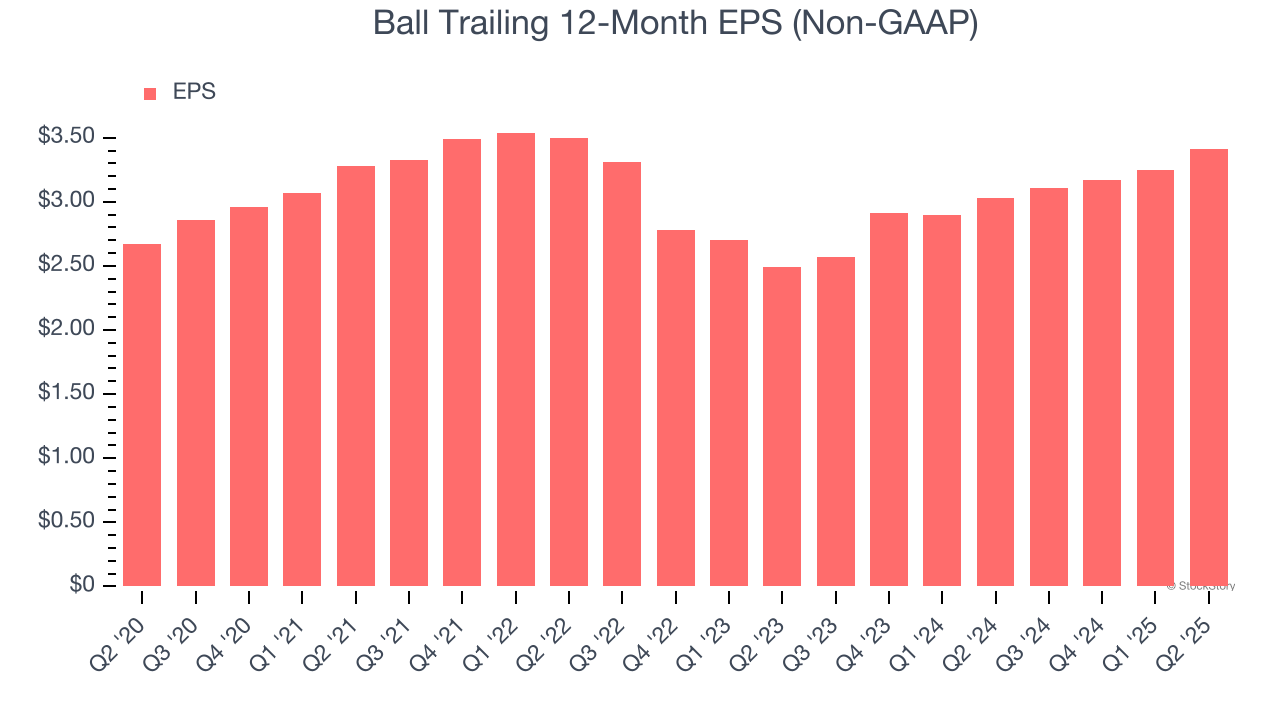

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Ball’s EPS grew at an unimpressive 5% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 1.9% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

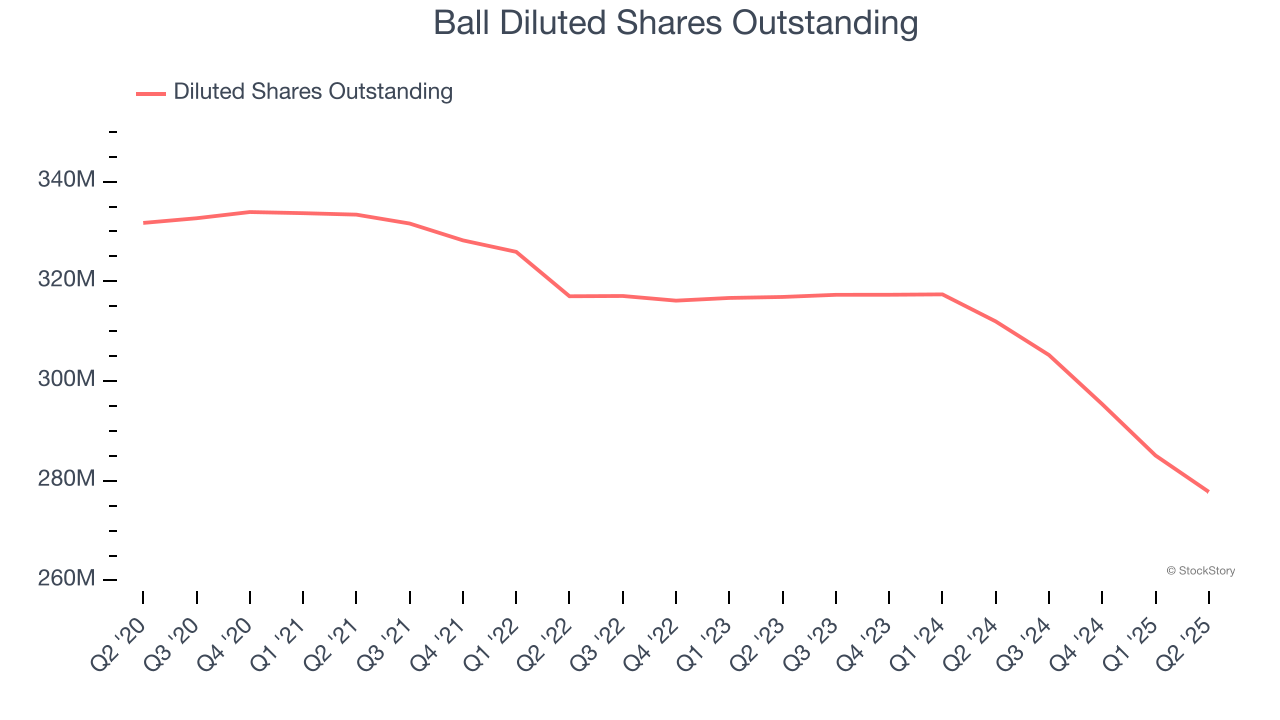

Diving into the nuances of Ball’s earnings can give us a better understanding of its performance. A five-year view shows that Ball has repurchased its stock, shrinking its share count by 16.3%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Ball, its two-year annual EPS growth of 17% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q2, Ball reported adjusted EPS at $0.90, up from $0.74 in the same quarter last year. This print beat analysts’ estimates by 3.8%. Over the next 12 months, Wall Street expects Ball’s full-year EPS of $3.41 to grow 10.6%.

Key Takeaways from Ball’s Q2 Results

We were impressed by how significantly Ball blew past analysts’ EBITDA expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 2.4% to $59.03 immediately after reporting.

Ball may have had a good quarter, but does that mean you should invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.