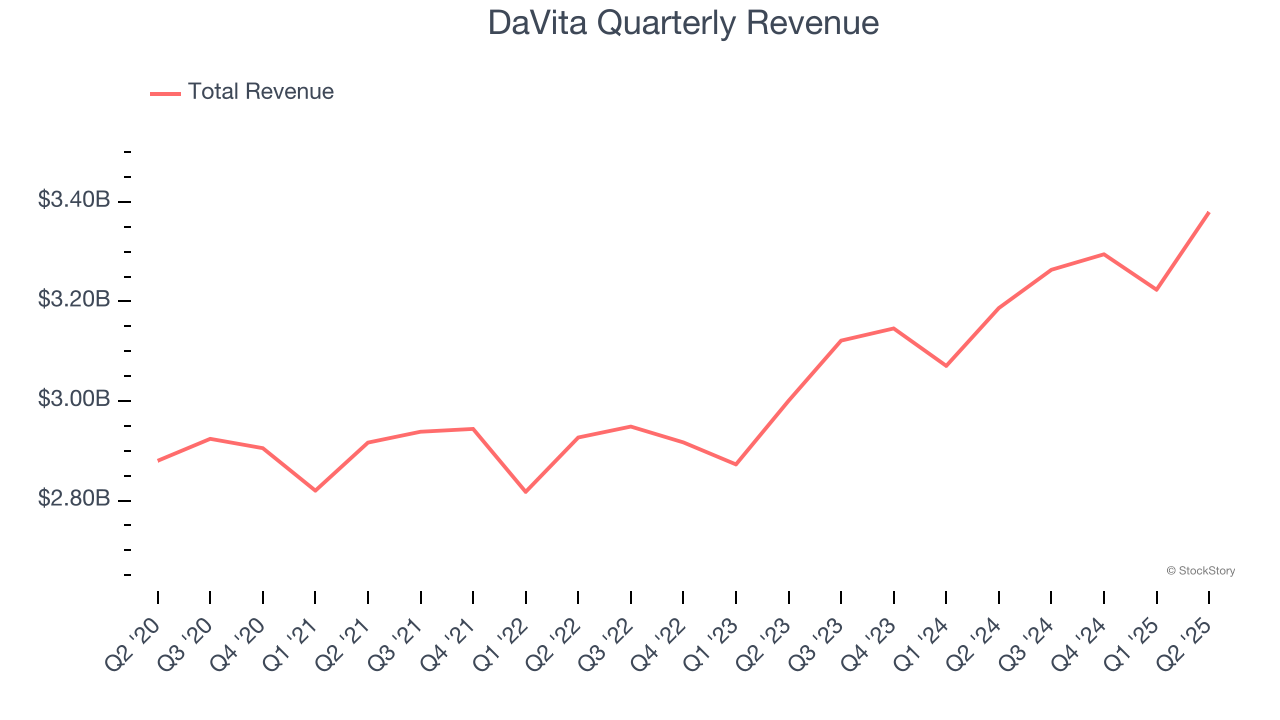

Dialysis provider DaVita Inc. (NYSE:DVA) announced better-than-expected revenue in Q2 CY2025, with sales up 6.1% year on year to $3.38 billion. Its non-GAAP profit of $2.95 per share was 7.3% above analysts’ consensus estimates.

Is now the time to buy DaVita? Find out by accessing our full research report, it’s free.

DaVita (DVA) Q2 CY2025 Highlights:

- Revenue: $3.38 billion vs analyst estimates of $3.36 billion (6.1% year-on-year growth, 0.7% beat)

- Adjusted EPS: $2.95 vs analyst estimates of $2.75 (7.3% beat)

- Adjusted EBITDA: $745.4 million vs analyst estimates of $707.9 million (22.1% margin, 5.3% beat)

- Management reiterated its full-year Adjusted EPS guidance of $10.75 at the midpoint

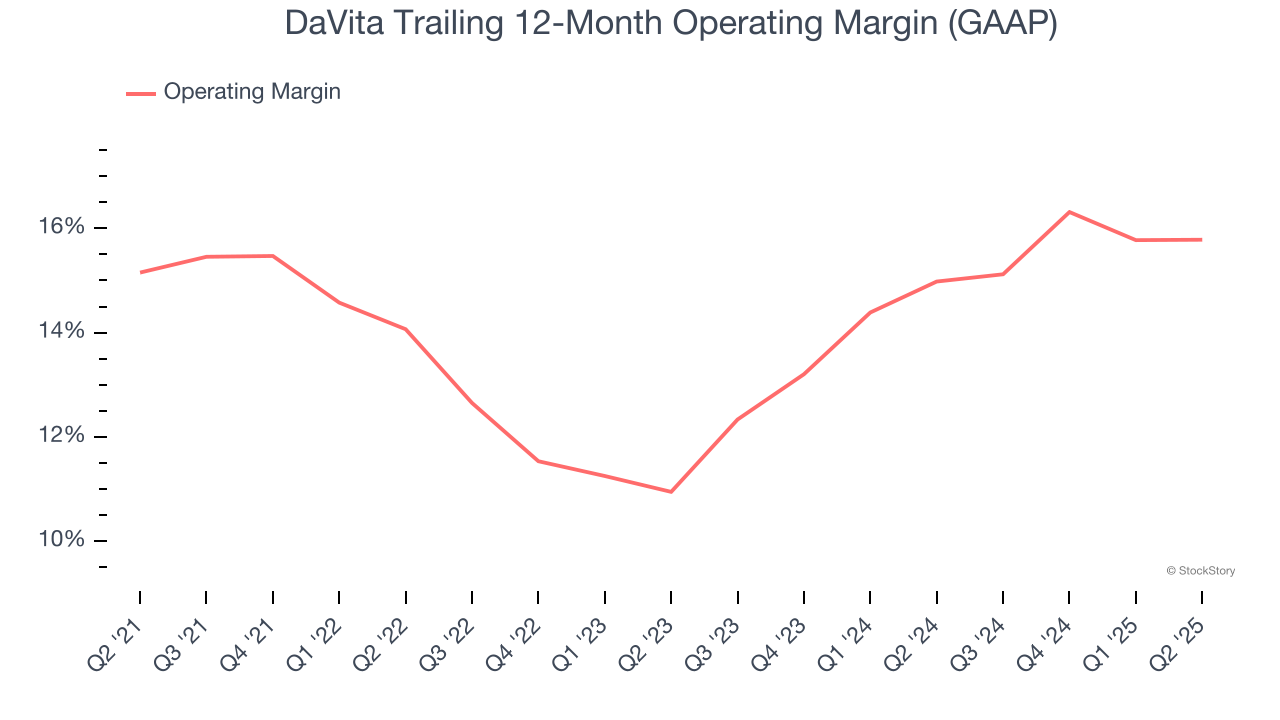

- Operating Margin: 15.9%, in line with the same quarter last year

- Free Cash Flow Margin: 6%, down from 21.2% in the same quarter last year

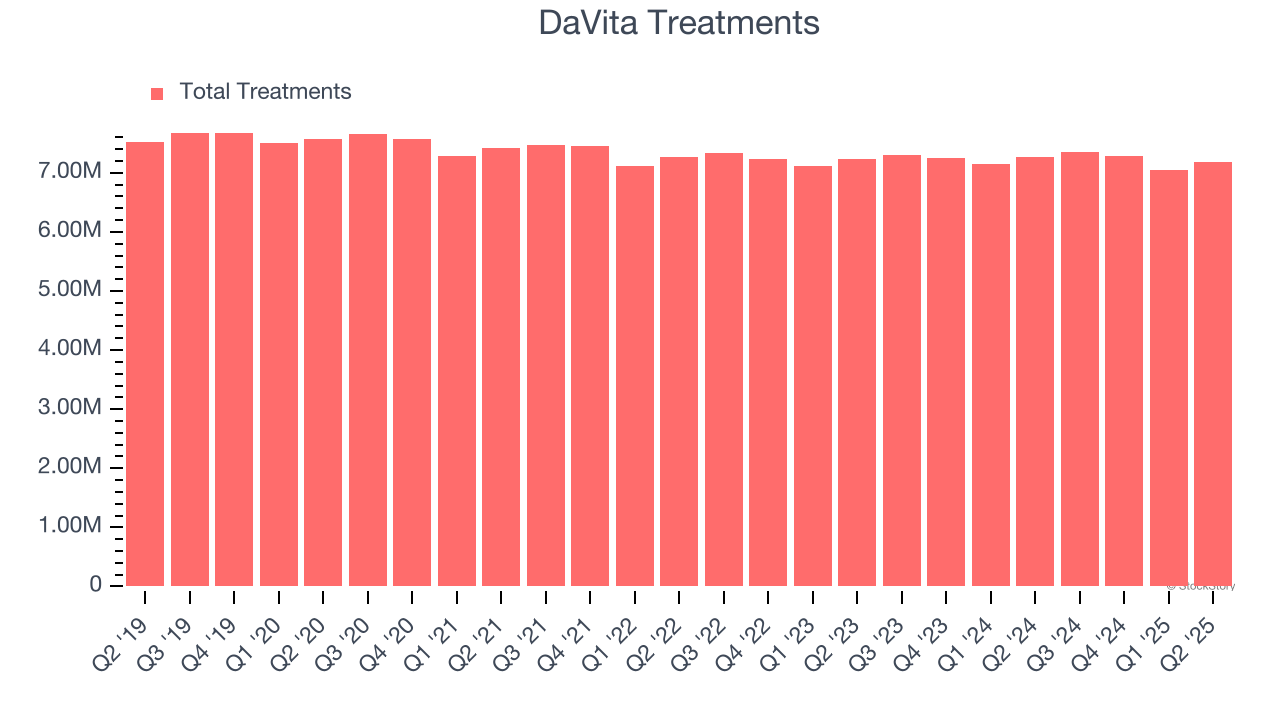

- Sales Volumes fell 1.1% year on year (0.5% in the same quarter last year)

- Market Capitalization: $10.53 billion

"We're reporting another solid quarter, fueled by our unwavering focus on patient care," said Javier Rodriguez, CEO of DaVita Inc.

Company Overview

With over 2,600 dialysis centers across the United States and a presence in 13 countries, DaVita (NYSE:DVA) operates a network of dialysis centers providing treatment and care for patients with chronic kidney disease and end-stage kidney disease.

Revenue Growth

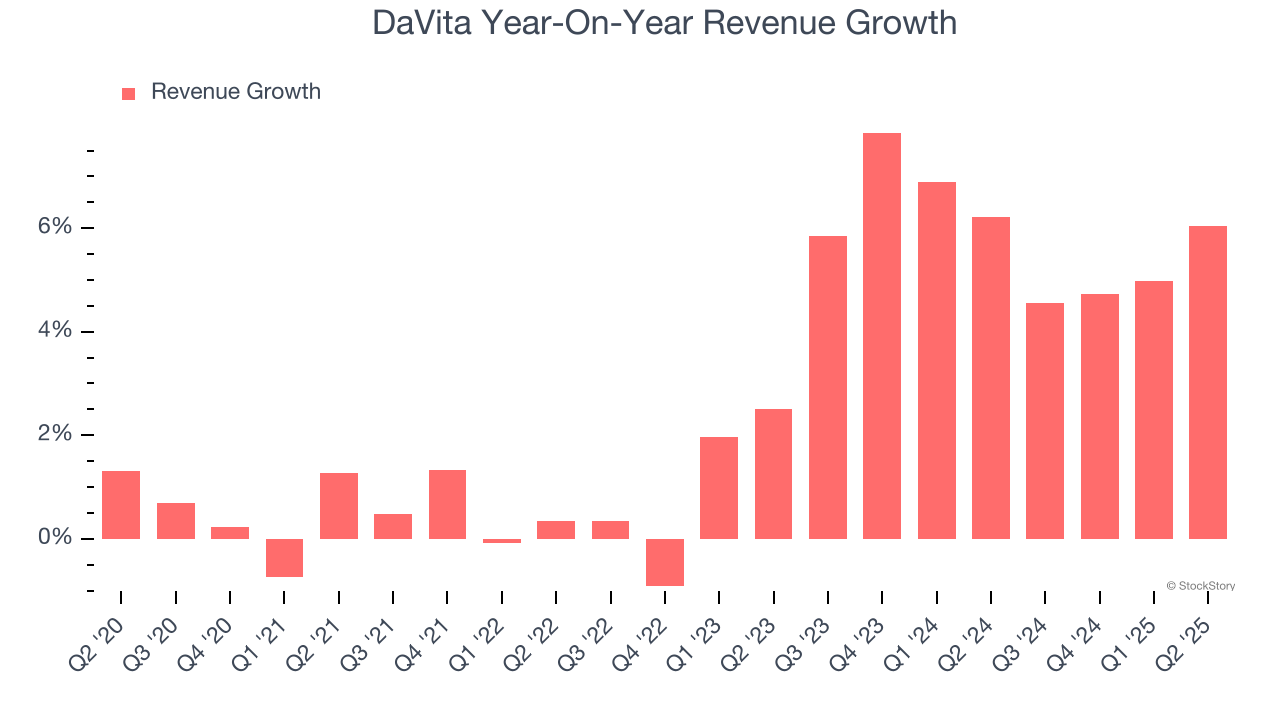

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, DaVita’s 2.7% annualized revenue growth over the last five years was tepid. This fell short of our benchmarks and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. DaVita’s annualized revenue growth of 5.9% over the last two years is above its five-year trend, but we were still disappointed by the results.

We can better understand the company’s revenue dynamics by analyzing its number of treatments, which reached 7.19 million in the latest quarter. Over the last two years, DaVita’s treatments were flat. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, DaVita reported year-on-year revenue growth of 6.1%, and its $3.38 billion of revenue exceeded Wall Street’s estimates by 0.7%.

Looking ahead, sell-side analysts expect revenue to grow 3.9% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

DaVita’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 14.2% over the last five years. This profitability was higher than the broader healthcare sector, showing it did a decent job managing its expenses.

Analyzing the trend in its profitability, DaVita’s operating margin of 15.8% for the trailing 12 months may be around the same as five years ago, but it has increased by 4.8 percentage points over the last two years.

In Q2, DaVita generated an operating margin profit margin of 15.9%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

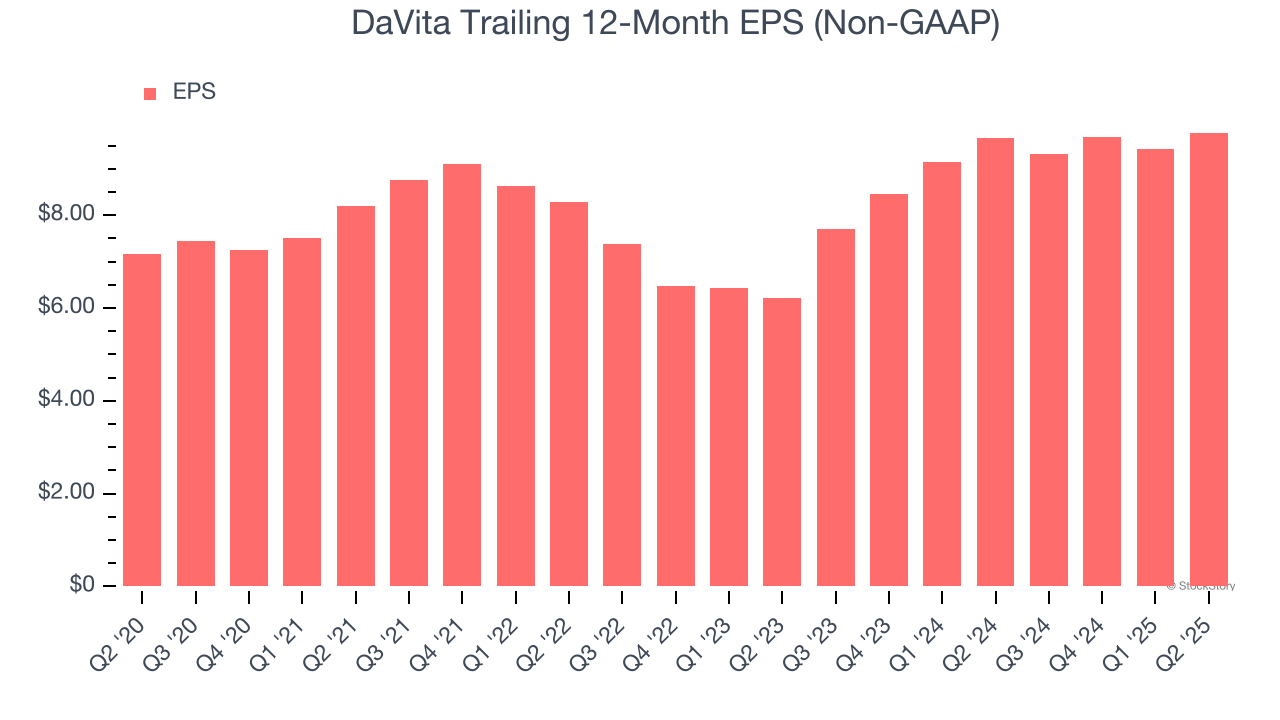

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

DaVita’s EPS grew at a decent 6.4% compounded annual growth rate over the last five years, higher than its 2.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

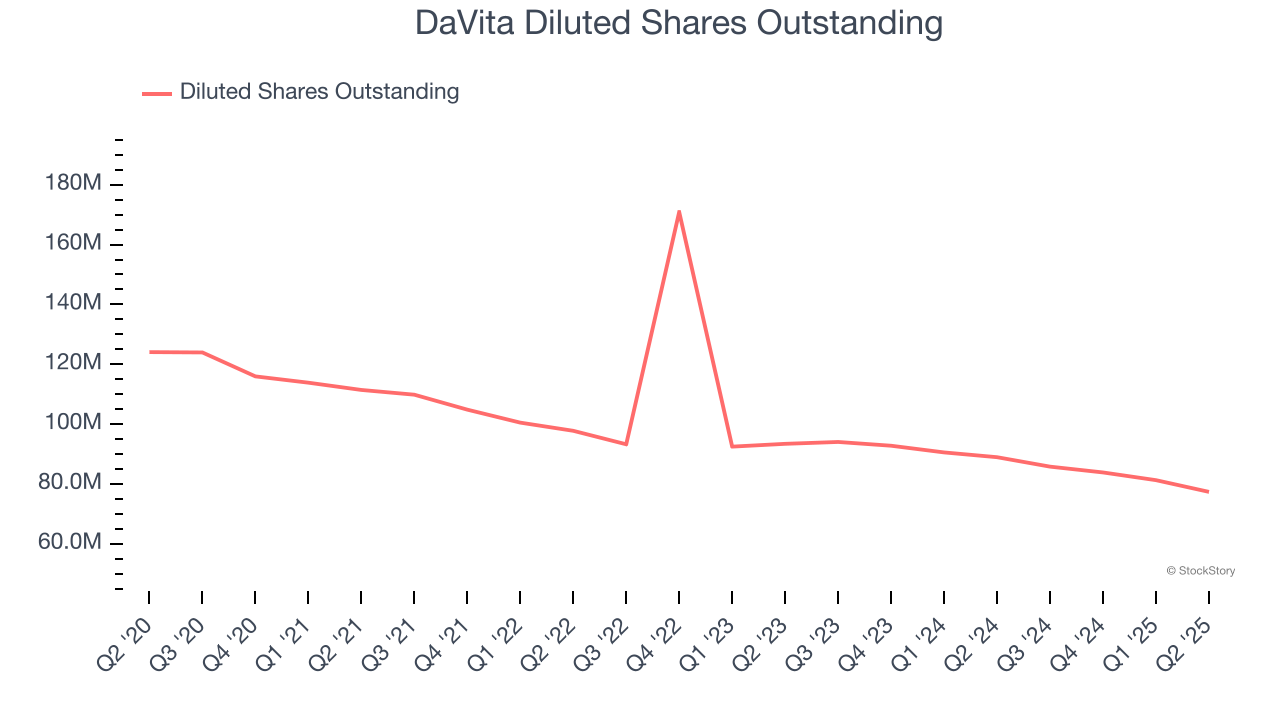

We can take a deeper look into DaVita’s earnings to better understand the drivers of its performance. A five-year view shows that DaVita has repurchased its stock, shrinking its share count by 37.6%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q2, DaVita reported adjusted EPS at $2.95, up from $2.59 in the same quarter last year. This print beat analysts’ estimates by 7.3%. Over the next 12 months, Wall Street expects DaVita’s full-year EPS of $9.78 to grow 20.2%.

Key Takeaways from DaVita’s Q2 Results

It was encouraging to see DaVita beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its sales volume slightly missed. Zooming out, we think this was a mixed quarter. Investors were likely hoping for more, and shares traded down 1.4% to $139 immediately following the results.

Is DaVita an attractive investment opportunity at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.