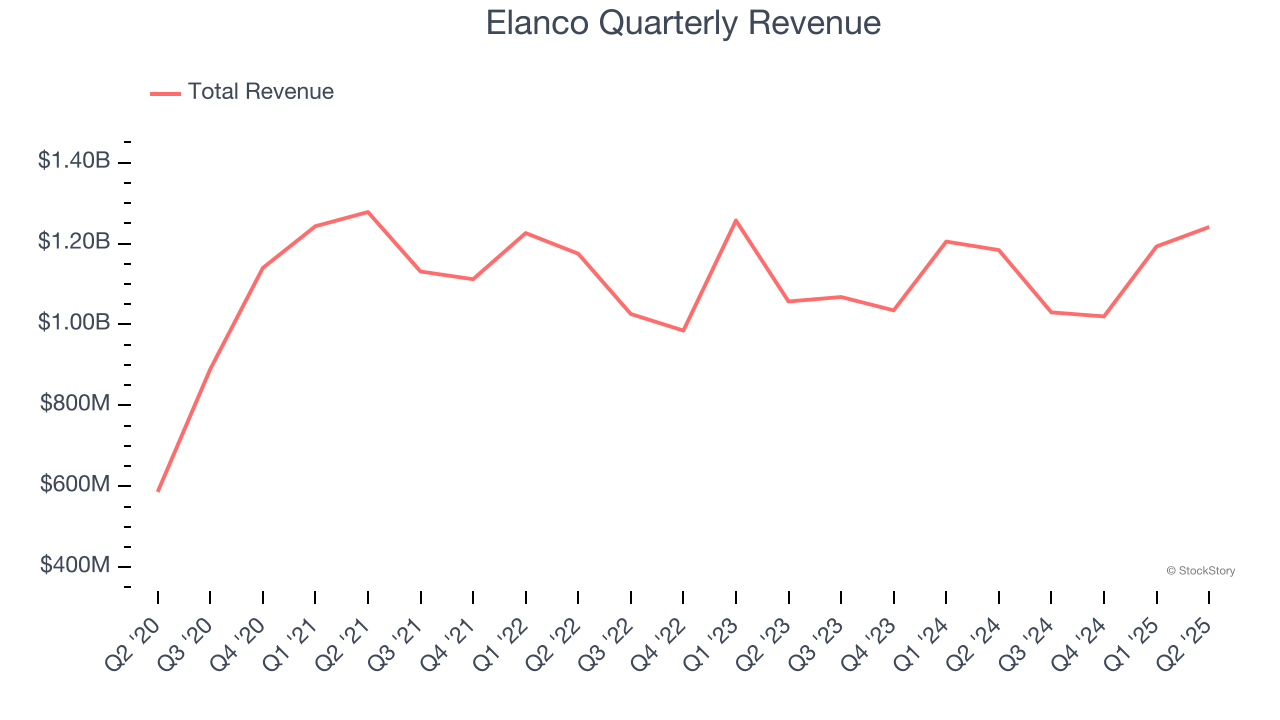

Animal health company Elanco (NYSE:ELAN) reported revenue ahead of Wall Street’s expectations in Q2 CY2025, with sales up 4.8% year on year to $1.24 billion. Guidance for next quarter’s revenue was better than expected at $1.1 billion at the midpoint, 0.9% above analysts’ estimates. Its non-GAAP profit of $0.26 per share was 29.5% above analysts’ consensus estimates.

Is now the time to buy Elanco? Find out by accessing our full research report, it’s free.

Elanco (ELAN) Q2 CY2025 Highlights:

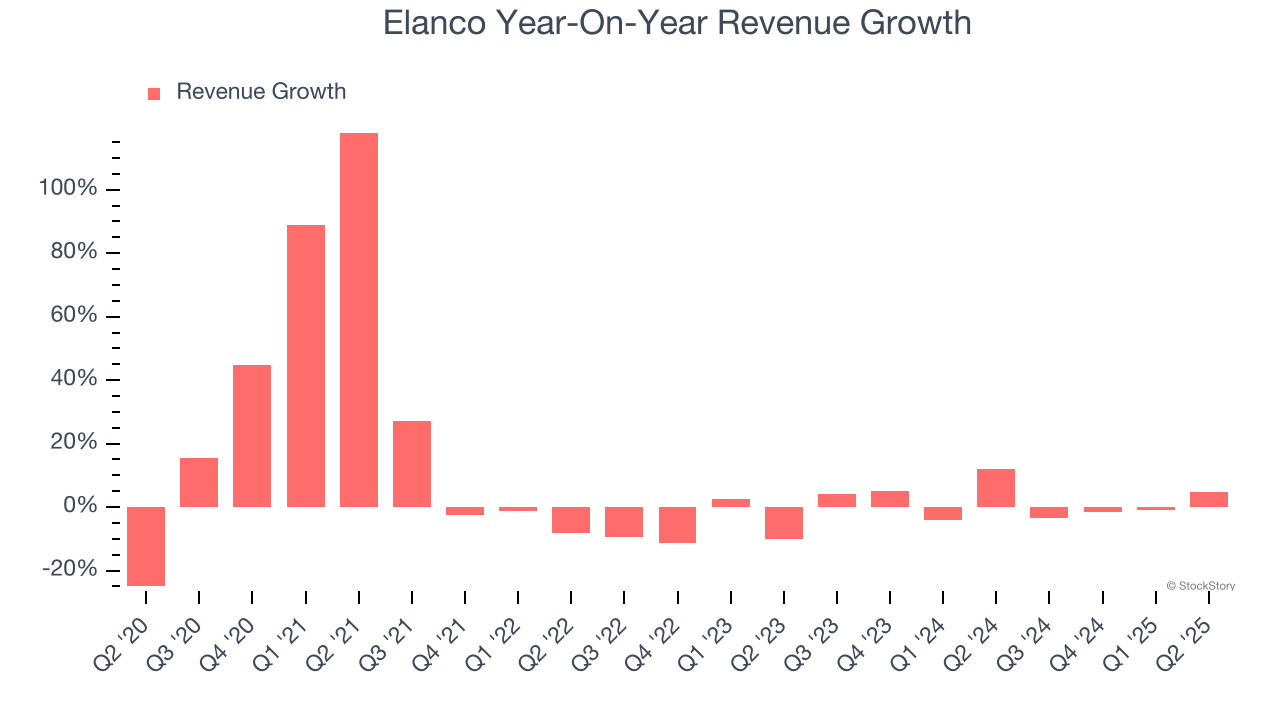

- Revenue: $1.24 billion vs analyst estimates of $1.19 billion (4.8% year-on-year growth, 4.7% beat)

- Adjusted EPS: $0.26 vs analyst estimates of $0.20 (29.5% beat)

- Adjusted EBITDA: $238 million vs analyst estimates of $216.9 million (19.2% margin, 9.8% beat)

- The company lifted its revenue guidance for the full year to $4.6 billion at the midpoint from $4.55 billion, a 1.1% increase

- Management raised its full-year Adjusted EPS guidance to $0.88 at the midpoint, a 6% increase

- EBITDA guidance for the full year is $870 million at the midpoint, in line with analyst expectations

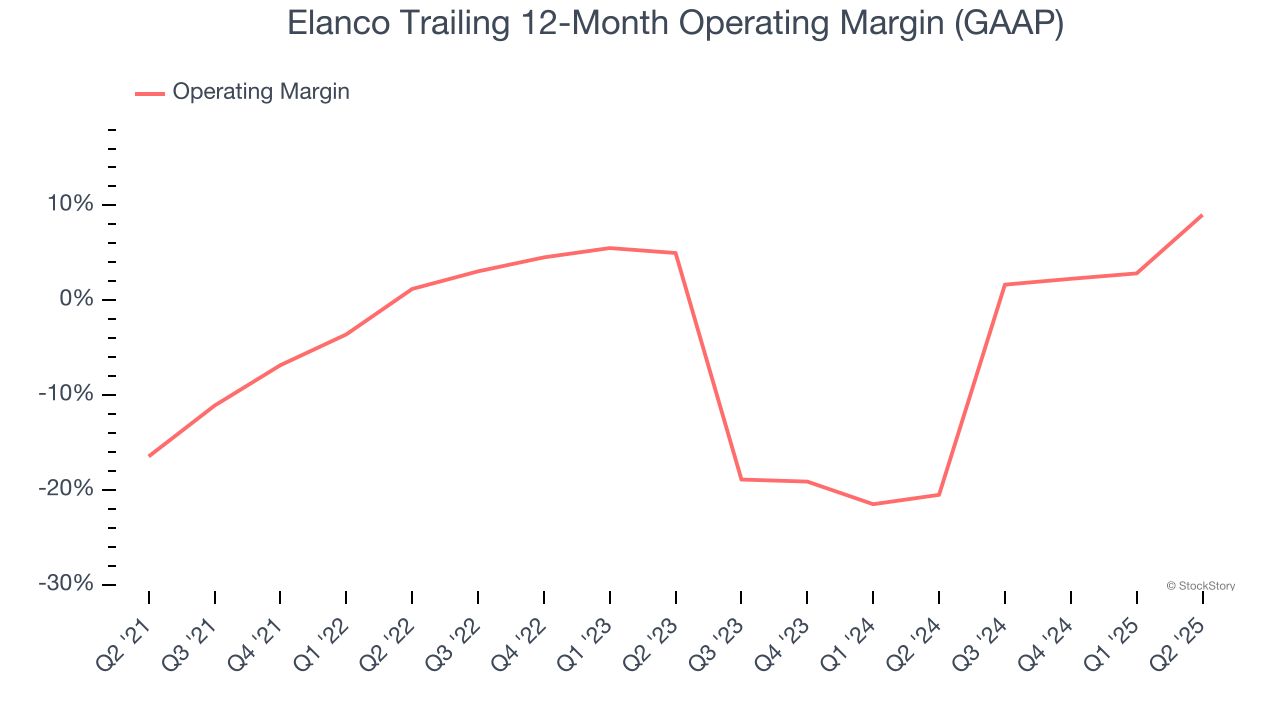

- Operating Margin: 25.2%, up from 3% in the same quarter last year

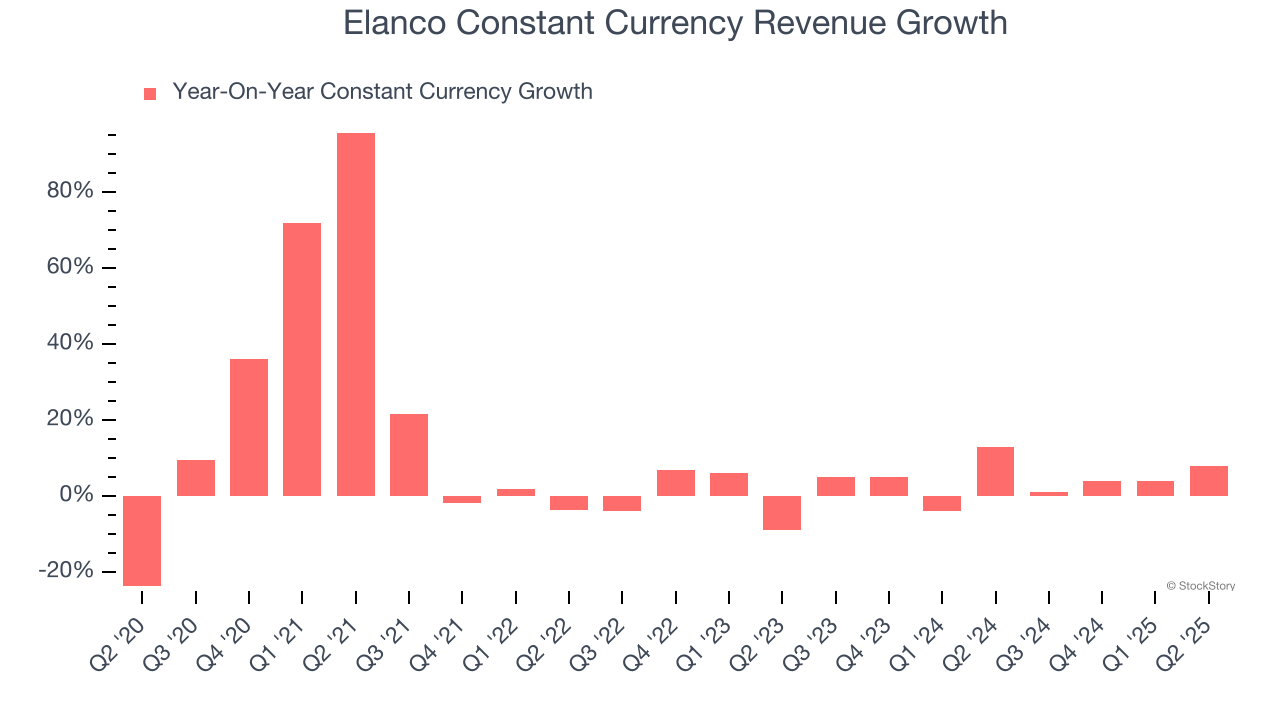

- Constant Currency Revenue rose 8% year on year (13% in the same quarter last year)

- Market Capitalization: $6.93 billion

"I'd like to thank our global Elanco team for delivering our 8th straight quarter of growth, driving results beyond expectations," said Jeff Simmons, President and CEO of Elanco.

Company Overview

Originally established as a division of pharmaceutical giant Eli Lilly before becoming independent in 2018, Elanco Animal Health (NYSE:ELAN) develops and sells medications, vaccines, and other health products for pets and farm animals across more than 90 countries.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Elanco’s sales grew at a decent 9.9% compounded annual growth rate over the last five years. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Elanco’s recent performance shows its demand has slowed as its annualized revenue growth of 1.8% over the last two years was below its five-year trend.

We can dig further into the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 4.5% year-on-year growth. Because this number is better than its normal revenue growth, we can see that foreign exchange rates have been a headwind for Elanco.

This quarter, Elanco reported modest year-on-year revenue growth of 4.8% but beat Wall Street’s estimates by 4.7%. Company management is currently guiding for a 6.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4% over the next 12 months. While this projection suggests its newer products and services will spur better top-line performance, it is still below average for the sector.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Although Elanco was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 4.4% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Elanco’s operating margin rose by 25.4 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 4 percentage points on a two-year basis.

This quarter, Elanco generated an operating margin profit margin of 25.2%, up 22.3 percentage points year on year. This increase was a welcome development and shows it was more efficient.

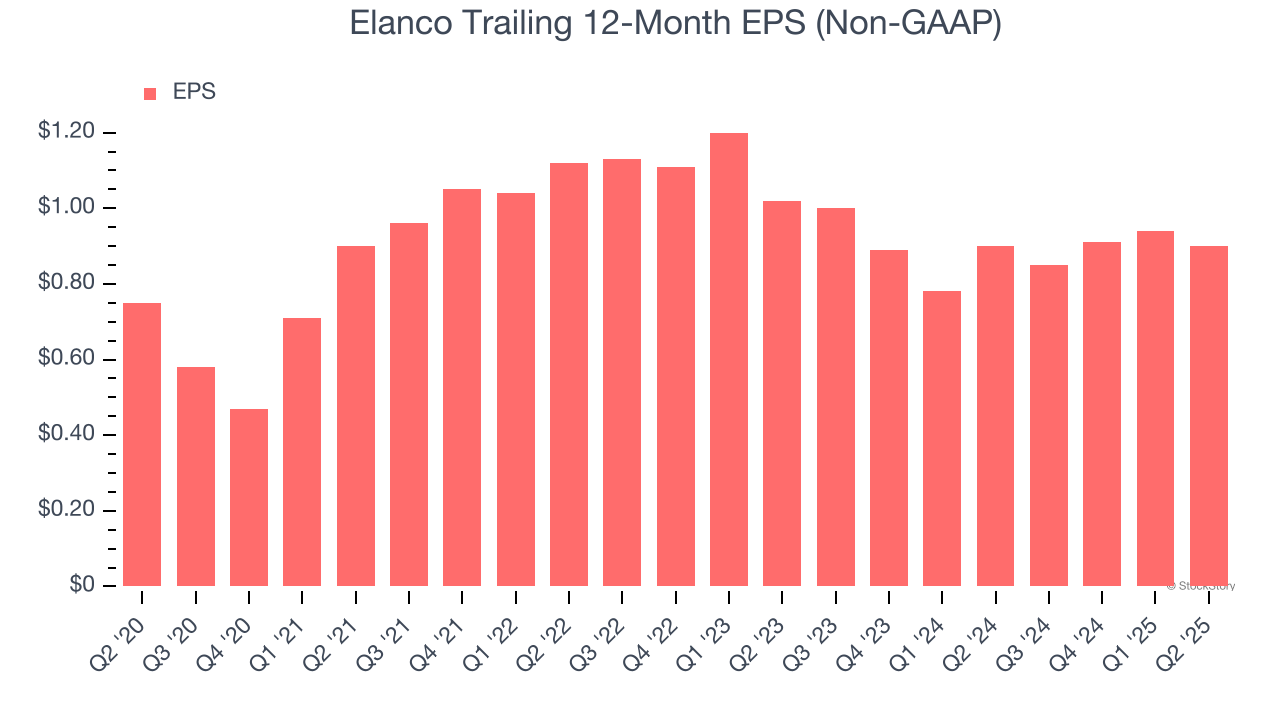

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Elanco’s EPS grew at an unimpressive 3.7% compounded annual growth rate over the last five years, lower than its 9.9% annualized revenue growth. However, its operating margin actually improved during this time, telling us that non-fundamental factors such as taxes affected its ultimate earnings.

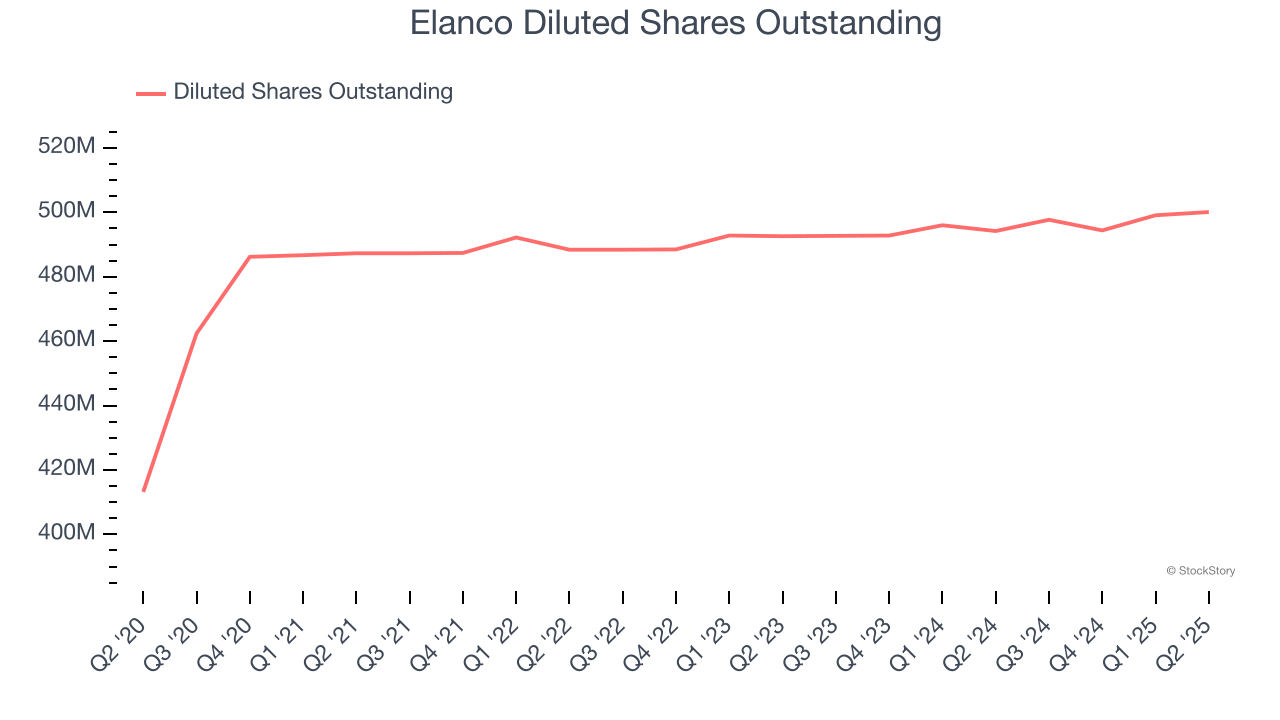

Diving into the nuances of Elanco’s earnings can give us a better understanding of its performance. A five-year view shows Elanco has diluted its shareholders, growing its share count by 21%. This dilution overshadowed its increased operating efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q2, Elanco reported adjusted EPS at $0.26, down from $0.30 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Elanco’s full-year EPS of $0.90 to shrink by 2.6%.

Key Takeaways from Elanco’s Q2 Results

We were impressed by how significantly Elanco blew past analysts’ constant currency revenue expectations this quarter. We were also excited its EPS outperformed Wall Street’s estimates by a wide margin. On the other hand, its EBITDA guidance for next quarter missed. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 15.4% to $16.13 immediately after reporting.

Elanco had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.